![]()

World Energy Outlook

By: Barbara Altizer

Coal Leader

|

Dr Jurgen Stadelhofer, Chair |

The International Energy Agency recently completed the 2004 World Energy Outlook which appears at an extremely volatile and uncertain time. Soaring oil, gas and coal prices, exploding energy demand in China, was in Iraq and electricity blackouts across the world are among the signs and causes of the profound transformations through which the energy world is passing.

SECTORAL DEMAND

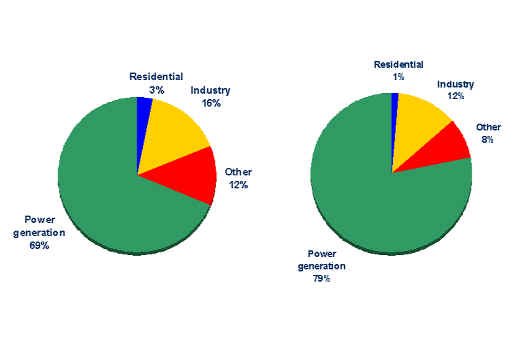

The utility sector's share of global coal demand will rise from 69% in 2002 to 79% by 2030. Despite this growth,

coal's share of global electricity production will decline slightly, from 39% at present to 38% in 2030. The main contributor to demand growth will be the rapid expansion of coal-fired generating capacity in China and other parts of developing Asia. Renewed interest in coal-fired power plants is also becoming apparent in several mature markets, particularly the United States, where the price of natural gas has risen sharply. In the long term, coal use in the power sector will be boosted by an assumed reduction in this price relative to gas, as well as by the gradual development and deployment of advanced coal technologies. The main impediment to investment in coal-fired capacity will be the cost of meeting climate change targets and other environmental requirements.

Industrial coal use, principally the use of coking coal for the manufacture of iron and still, will increase by 0.5% per year over the projection period. This modest growth reflects increased use of recycled steel and continuing improvements in the efficiency of iron production and blast furnace technology.

As with steam coal, growth in the coking coal market will be most robust in developing Asian countries, where construction, car production and demand for household appliances will increase as incomes rise. Demand for coking coal will continue to decline in the OECD, as it has since the

1980's, as coke and pig iron production shifts to developing regions. Coal for industrial and residential heating will continue to lose market share to gas.

|

IMPACT OF ENVIRONMENTAL POLICY AND TECHNOLOGY

The main uncertainty surrounding the outlook for coal demand in OECD regions is the impact of government policies and measures to address environmental concerns. (See Chart on Page 8). Typical existing coal-fired power plants emit more pollutants and more carbon dioxide than do oil or natural gas-fired plants. Partly because of such uncertainty, few coal-fired power stations have been built in recent years in developed countries outside Asia. Potential investors have shied away from coal-fired power stations and boilers for fear that new environmental rules could limit their use and increase costs.

Implementation of clean coal technologies (CCT), which would improve the thermal efficiency of coal production and use and reduce emissions, could minimize investment risks and give a major boost to the prospects for coal demand. While attention is usually focused on power generation technologies, continuous technological advances are being made along the entire coal chain. New techniques have been developed for coal mining and the preparation of coal for use in power stations, as well as for coal combustion, emissions control and the disposal of solid waste. Technologies on the horizon such as carbon capture and storage could achieve near-zero emissions of all pollutants from coal-fired power plants.

Cost is the major barrier to the adoption of clean coal technologies. Government actions, including increased research and development, could help reduce costs. If they do, coal could remain a low-cost source of electricity generation in a carbon-constrained environment.

Because of the long life of coal-fired power plants and boilers, and the higher cost of building advanced plants, new infrastructure will come into operation only very gradually. Large numbers of conventional plants are still being built, and many existing conventional plants are being retrofitted with equipment to limit emissions and extend the plants

economic lives.

| World Coal Demand by Sector | ||

|

COAL RESERVES AND PRODUCTION

Proven coal reserves worldwide total 907 billion tonnes or almost 200 years of production at current rates. In energy equivalent terms, this exceeds the combined proven reserves of both oil and gas by a very wide margin. Hard coal, coking coal and steam coal, makes up 83% of proven reserves. The rest is brown coal.

Countries, which rely heavily on coal for domestic needs or export revenue generally, have large reserves of coal. The reason for this is that as coal production, consumption and transportation infrastructure expands, resources in proximity to already exploited reserves often become economically viable and enter the proven reserve classification. The largest reserves are found in the United States, Russia, and China. Although steam coal reserves are widespread, mining costs and quality vary. Coking coal reserves are widespread, mining costs and qualities vary. Coking coal reserves are more limited, with the best-quality deposits found in the United States, Australia, Canada, and China. Brown coal is typically used by power plants situated close to where the coal is mined, because its energy content is low and it is costly and difficult to transport.

PRODUCTION PROSPECTS

Global coal production will increase by 1.4% per annum over the Outlook period, reaching 7 billion tonnes in 2030. China will reinforce its position as the

world's leading producer, accounting for around half the increase in global output over the period. The other major producers in 2030 will be the United States, India, and Australia. Coal production in Europe will continue to decline as subsidies are reduced and uncompetitive mines are closed.

Some 80% of incremental coal production during 2003-2030 will be steam coal. By 2030, steam coal production will reach 5, 212 Mt, compared with 3, 417 Mt in 2002 to 624 Mt in 2030. Coking coal production will become increasingly concentrated in China and Australia. These countries will account for about 60% of global supply in 2030. Brown coal production will increase at a rate of 1.1% per year, reaching 1,175 Mt in 2030.

HARD GOAL TRADE

The volume of hard coal traded internationally will increase steadily to 2030. Main drivers of the increase will be continuing industrialization of developing Asian countries and the decline of coal mining in Europe, which will provide enlarged markets for exporters. Total trade is expected to increase from 688 Mt in 2002 to 1,063 Mt in 2030. Regional trade patterns and the breakdown of trade by coal type will change markedly.

As a share of total hard coal demand, trade has increased rapidly, from 10% in the early 1990s to 17% in 2002. By 2030, this share is expected to have risen slightly more, to 18%. Although some regions will import more of their coal needs, much of the increase in production in major producing regions, including China, North America, and India, will be destined for domestic markets.

|

FutureGen: Zero-Emission Technologies Coal-fired power stations can emit several noxious pollutants including particulates, mercury and sulfur and nitrogen oxides. It is now thought technically possible virtually to eliminate all these emissions, as well as those of carbon dioxide. |

The share of steam coal in world coal trade will continue to rise, stimulated by strong demand from electricity generators in Asia and by a growing need for imports in Europe. By 2030 trade in steam coal will account for 76% of total hard coal trade versus 69% now. Trade in coking coal will grow slowly, reflecting the growing use of steel-making technologies such as pulverized coal injection (which uses steam coal quality), the application of advanced steel-making technologies not requiring high-quality coking coal, such as direct smelting and ongoing steel recycling.

Because transport costs account for a large share of the total delivered price of coal, international trade in steam coal is effectively divided into two regional markets

- the Atlantic and the Pacific. Markets overlap when prices are high and supplies are plentiful. South Africa is the natural point of convergence of the two markets and plays an important role in transmitting price signals between them.

The Atlantic market is made up of importing countries in Western Europe, notably the United Kingdom, Germany, and Spain. The Pacific market consists of developing and OECD Asian importers, notable Japan, Korea, and Chinese Taipei. The Pacific market currently accounts for about 60% of world steam coal trade. Through the Outlook period, it is expected that the Pacific market will be supplied mainly by Australia, Indonesia, and China. South Africa, the United States, Colombia, and Venezuela will be the primary supplying Europe, Asia, and the Americas.

Sources of internationally traded coking coal will remain limited. Australia is by far the largest current supplier, accounting for 51% of world exports in 2002. The United States and Canada are also significant exporters. Recently, China has also emerged as an important supplier of coking coal to world markets. Because coking coal is more expensive than steam coal, Australia can afford the high freight costs involved in exporting it around the globe. Growth is coking coal trade will be led by the needs of the Asian steel industry.

PRICE DEVELOPMENTS

Since 2003, coal prices around the world have risen sharply after having moved in a fairly narrow band through the preceding decade. The spot price of steam coal delivered to northwest Europe jumped from around $36 per tonne in January 2003 to $79 in July 2004. Contract prices, which are typically well below spot prices, have risen less. In the Reference Scenario, the IEA steam coal import price averaged $38 per tonne in 2003 ($41/t in nominal terms). Prices are assumed to increase into 2005 before falling back to and stabilize at around $40 until 2010. After that, we assume they will rise slowly and in a linear fashion, reaching $44 in 2030. The increase is, nonetheless, slower than those of oil or gas. Rising oil prices will raise the cost of transporting coal and also make it more competitive for industrial users and power generators. This factor is assumed to offset an expected reduction in the cost of mining coal, as low-cost countries continue to rationalize their industries.

Strong demand has been the primary cause of the recent jump in prices. World coal consumption increased by close to 7% in 2003 (BP, 2004). Demand increased most sharply in China, where industrial production and electricity demand are both booming. In Japan, the unscheduled closure of several nuclear reactors has increased the use of coal in power generation. Coal producers have been hard pressed to respond to increased demand. In North America, coal mines are currently operating at close to full capacity as in recent years there has been little expansion of new production capacity and a slowdown in the rate of productivity improvements. Upward pressure on prices has been further compounded by Chinese government restrictions on coal exports to ensure that domestic needs are met.

Another factor in the recent price rise has been a dramatic increase in maritime freight rates. The cost of transporting coal from the port of Newcastle in Australia to Japan rose from around $4.5 per ton in January 2002 to over $22 during February 2004. .Freight rates have since subsided but remain at historically high levels. An important factoring the run-up in freight rates was

China's huge demand for imports of commodities such as iron ore, which compete directly with coal for space on dry-bulk cargoes. In 2002, coal accounted for about 42% of the world's seaborne dry-bulk trade. A further contributing factor to high freight rates has been bottlenecks at some major coal-loading ports. The appreciation of the currencies of several major coal-exporting countries, especially the Australian dollar and the South African rand, has also contributed to higher prices denominated in U.S. dollars.

INVESTMENT OUTLOOK

Cumulative investment needs in the global coal industry, including financing for mining, shipping and ports, are expected to be just under $400 billion over the period 2003-2030 This much will be needed to replace production capacity that will close during the period, to meet rising demand and to accommodate growing trade. If investment in coal-fired power generating capacity is included, investment needs increase to $1.7 trillion.

Investment requirements will be increasingly concentrated in developing Asian countries. China alone will account for $129 billion, over 35% of the global total. This is just slightly more than the combined investment requirements in non-OECD countries. Around 8% of the investment in non-OECD countries will go to supply infrastructure to export coal to the OECD.

Investment in mining, at around $350 billion, represents close to 90% of the

projected total. Investment in the dry-bulk cargo fleet (for coal transportation) will amount to $34 billion,and coal-related investments in ports will be $13 billion.

Advanced technologies now available and under development could dramatically alter investment patterns by boosting coal demand, particularly in OECD regions. In the Pacific market, Japan is the only major coal user with a commitment to cut its carbon dioxide emissions under the Kyoto Protocol. Other countries in the region often place a relatively higher value on economic growth and security of supply than on environmental objectives. As a result, coal use in the region is likely to remain strong

regardless of changes in technology.

REGIONAL TRENDS

OECD North America

OECD North America is expected to remain the world's second-largest coal market in 2030, after China. By that time, coal will account for 18% of the region's total energy needs, down from 21% in 2002. Demand will rise by a mere 0.5% per year, from 1,051 Mt to 1,222 Mt, over the projection period. In 2003, the region consumed a record level of coal and for the first time ever, produced less coal than it consumed.

Coal use will be driven mainly by the needs of the power sector and by the prices of alternative fuels. Demand will be encouraged by the rising cost and reduced availability of natural gas, particularly in the United States. By 2030, coal is expected to fuel 40% of the region's power generation compared to 46% in 2002. The region's demand for coking coal will increase at a modest 0.8% per annum thanks to efficiency gains and technological changes in steel manufacturing.

Most North American coal demand will be met domestically. The combined proven coal reserves of the United States, Canada, and Mexico amount to 254 billion tons - more than a quarter of the world total. In recent years in the United States, there has been a trend towards increasing coal production in the western states. This follows on from the strict sulfur dioxide emission limits for power pants introduced in 1995 by the Clear Air Act. Coals mined in the western states tend to have lower sulfur content than those found in the eastern states reducing the need for investment in flue gas desulphurization.

The United States was the largest coal exporter in the world from 1984 until the early 1990's, but its exports have since fallen precipitously in the face of competition from lower-cost producers in South America, South Africa, and Australia. United States reserves of export-quality are declining and domestic markets are absorbing most of the remaining low-sulfur coal. Reserves of export-quality coal are extensive in some areas, but they are located far from ports for shipment to export markets. Both the United States and Canada are expected to continue to play an important, yet diminishing, role in supplying high-quality coking coal to the steel industry, particularly in Europe. Their share of the global coking coal market is expected to fall from 21% to 14% over the projection period.

|

Coal Industry Investment

Almost all Coal Investment will be for Mining

- |

OECD EUROPE

Coal demand in OECD Europe will increase slowly in the first half of the Outlook period and then decline in the later years. Demand is expected to be 816 Mt in 2002. Coal will continue to lose market share to natural gas in the power sector if gas prices remain relatively low and stable, and if gas supply is secure. The relative cost of coal will also be influenced by environmental policies.

OECD Europe's proven coal reserves total 39 billion tons or about 4% of the world total. Around forty per cent of these reserves is brown coal. In most cases, Europe's hard coal reserves are expensive to mine. Estimates of European coal reserves have been revised downwards by more than 60% since the end of 1999 following an economic re-evaluation of what makes a viable mine. The largest downgrades have occurred in Germany and to a lesser extent in Poland. Coal production in OECD European countries has declined significantly since 1990, from around 1,036 Mt to 647 Mt in 2002. The largest decline occurred in Germany, where output fell by 230 Mt between 1990 and 2002. Production dropped by 62 Mt in the United Kingdom, 54 Mt in Poland and 48 Mt in the Czech Republic over the same period. The fall in production from European coalmines has exceeded a parallel slump in demand. Imports have risen and this trend is set to continue, with imports projected to grow 268 Mt in 2030. The share of imports in total coal demand will increase from 27% in 2002 to 33% in 2030.

Much of the region's brown coal production is commercially competitive and, with a few exceptions,, unsubsidized. In contrast, most European hard coal production remains uneconomic and depends on subsidies or other forms of protection. Subsidies are being phased out gradually in most European countries, although some of them may be retained on the grounds of security of energy supply. This will allow some high-cost mining capacity to be maintained, especially in Germany and Spain.

Two of the ten new members of the European Union, Poland and the Czech Republic, have large coal industries. Poland's hard coal production exceeds the total production of the 15 countries that made up the Union before the new members joined. The coal industries in both Poland and the Czech Republic have undergone considerable restructuring since the collapse of communism in 1989. Production has been cut and unprofitable pits closed. The process continues, and coal subsidies in the two countries are expected to be phased out slowly.

OECD PACIFIC

Coal demand in the OCED Pacific region will increase from 364 Mt in 2002 to 423 Mt in 2030, at an annual rate of growth of 0.5%. Prospects vary through the region. Japan will use slightly less coal in 2030 than it does today. But this will be more than offset by robust growth in Korea and slow growth in Australia and New Zealand. In all OECD Pacific countries, use of steam coal for power generation will be the main driver of increasing demand.

Australia is the only significant coal producer in the region. It is currently the world's largest exporter and sixth-largest producer. With 78 billion tons of proven coal reserves, and excellent rail and port infrastructure, Australia has the potential to greatly increase steam coal exports to the Pacific market. The extent to which Australian producers increase production to meet growth in Asian demand will depend largely on developments in China, which has emerged in recent years as a major exporter. Chinese exports are expected to continue to grow, but more slowly than in the recent past because of increasing domestic demand. Australia is projected to account for 26% of world steam coal trade in 2030, up from 21% in 2002.

Australia will face less competition in the coking coal market, where is is expected to extend its position as the leading exporter in both the Atlantic and Pacific markets. Australia's share of world coking coal exports is projected to reach 58% in 2030, up from around 50% in 2002.

Despite a projected decline in its consumption, Japan will remain the world's largest importer of coking coal, and, as with Korea, among the world's largest importers of steam coal. By 2030, Japanese coal imports will account for 13% of total world coal trade, down from 24% in 2002. Although Chinese producers have been gaining market share in Korea in recent years, much of the country's future demand is expected to be supplied from Australia.

CHINA

Chinese primary coal demand will grow from 1, 308 Mt in 2002 to 2, 402 Mt in 2030, an increase of 2.2% per year. China will thus extend its position as the world's largest coal consumer. Although coal will remain the dominant fuel in China's energy mix, its share of total primary energy consumption will drop from 57% in 2002 to 53% in 2030, owing to the growing use of natural gas in electricity generation and of oil in transportation.

The power sector will account for more than 73% of total Chinese coal consumption in 2030, compared with 52% in 2002, as coal remains the backbone of China's generating capacity. Industrial uses, mainly of coking coal in steel production, will rise at a more modest 0.7% per year. In response to rising incomes and urbanization, coal use in the residential sector will decline as it loses out to more convenient and cleaner sources of energy.

China has an estimated 114 billion tons of proven coal reserves. The majority of these are found in northern China, particularly in the provinces of Hebei, Shaanxi, and Inner Mongolia. Hard coal accounts for 84% of total proven reserves. The remainder consists of lower-quality coals, including lignite. China will remain the world's biggest producer of both steam and coking coal in 2030. In 2002, production totaled 1,398 Mt, around 29% of the world total. It is projected to increase to 2,490 Mt in 2030, or 35% of the world total.

The Chinese coal industry has undergone a major rationalization involving the

closure thousands of small mines, as well as, the expansion of large mines operated by the central government. This program has helped raise productivity levels, improved safety standards and given the government more control over production. Nonetheless, further reforms are needed. Illegal small-scale mining operations continue to pose problems; safety standards remain low and regulations are poorly applied. In addition, large state-owned mines are burdened with a wide range of social responsibilities, such as providing schools and hospitals, which distract management and undermine efficiency. The sector requires more investment, not only to expand capacity but also to modernize existing mines. Priorities include mechanizing underground mines, building coal-preparation plants and improving rail transport, water supply and water-disposal facilities.

China is an important, yet unpredictable, supplier of coal to world markets. China's exports totaled 97 Mt in 2002, making it the world's second-largest exporter after Australia. Exports are expected to increase steadily to 130 Mt in 2030. Currently, however, exports are being restricted by the government to alleviate local shortages of coal for electricity generation and steel production. Restrictions include a reduction in export price rebates and lowered export quotas. The export cap for 2004 is expected to be 80 Mt. These moves have disrupted world markets and raise prices, hitting European steel manufacturers particularly hard. Over the long term, however, China is expected to exploit its vast reserve base and its proximity to rapidly growing Asian markets to wind market share away from more distant suppliers. Export prospects will depend to a large extent on whether the government continues to support coal producers. Other factors will be the development of rail and port infrastructure and the rate of growth in domestic demand.

|

Non-Physical Trading of Steam Coal Steam coal is increasingly traded on electronic trading platforms. Compared with oil and as, this method of trading has been slow to develop, largely because power generators require a detailed assessment of coal specifications, often necessitating pilot testing, prior to use. The quality and other conditions for traded coal has alleviated this constraint. Improved coal indexes have also enabled trading in derivatives, which has increased market transparency, enabled coal producers and customers to hedge their floating price exposure and allowed speculation on future price movements. Derivatives are now largely used to set the spot price for steam coal in the Atlantic market. |

Because of its vast coal reserves and increasing reliance on foreign crude oil imports, China's interest in developing projects that convert coal into synthetic liquid fuel is growing. Under a recent agreement, South African's Sasol, in partnership with a number of Chinese companies, plans to develop two large coal-to-liquids plants in coal-rich Ningxia and Shaanxi provinces. If these projects proceed as hoped, their conbined capacity will amount to 60 Mt of oil per year. Sasol is the only company in the world currently operating commercial coal-to-liquids plants. Capital costs for such plants are much higher than costs for conventional oil projects and even for gas-to-liquids projects, but operating costs are moderate, particularly in the light of current world oil prices and if low-cost coal feedstocks are available. To reduce costs, China has established a centre in Shanghai to study new liquefaction techniques.

INDIA

Coal will remain the dominant fuel in India's energy mix through 2030. Demand is projected to grow from 391 Mt in 2002 to 758 Mt in 2030, at an average rate of growth of 2.4% per year. Only China's demand for coal will outstrip India's in the Outlook period. As in other regions, the power sector will be the chief driver of Indian demand. Currently, 71% of India's electricity is generated from coal. This share will decline to 64% by 2030.

India's coal needs will be largely met domestically. Production totaled 364 Mt in 2002, and is projected to increase to 705 Mt in 2030. India has 92.4 billion tons of proven coal reserves, 10% of the world total. Coal is located mainly in the centre and east of the country, far from the main consuming areas. As a result, large quantities of coal have to be transported by rail over long distances. Smaller amounts are shipped by a combination of rail and sea, at very high cost. This has encouraged growth in coal imports into certain coastal areas in recent years. India imports much of its coking coal needs as indigenous supplies are of a low quality due to their high ash content and low calorific value.

Productivity in Indian coal mines is well below international standards, because of low levels of mechanization and poor mine design. Investment is urgently needed along the whole coal chain from production to use. But the dire financial condition of the state electricity generators, the main users of coal in India, is holding back investment in coal-fired stations. Some electricity pricing reforms have been implemented, but much more needs to be done. Further liberalization of the domestic coal market it also needed, including the removal of impediments to foreign investment. Competition from imported coal could be a stimulus to improving performance in the domestic industry and to raising its attractiveness for investors.

AFRICA

African coal demand is expected to increase at an average annual rate of 1.5%, from 174 Mt in 2002 to 264 Mt in 2030. Africa has about 50.3 billion tons of proven coal reserves, or around 6% of the world total. South Africa accounts for the majority of both reserves and production on the continent. It produced around 223 Mt in 2002, over 95% of the African total. South Africa is the world's largest producer of coal-based synthetic liquid fuels. This market accounted for about 21% of the country's total coal consumption in 2002.

South Africa was the world's fourth-largest coal exporter in 2002. Exports, mostly of steam coal, totaled 70 Mt, most of which went to Europe. Europe has become an even more vital market for South African steam coal in recent years as exports may taper off in the long term, because of the country's limited reserves of export-quality coal. About 90% of exports are handled by the Richards Bay Coal Terminal, which is now operating at close to full capacity, but the terminal is currently being enlarged. We expect coal exports from Africa to total 110 Mt in 2030, or around 10% of world coal trade, the majority of which will continue to go to the European Union.

INDONESIA

Indonesia, the world's fourth most populous nation, will fulfill an important role in the coal market, particularly in the Asia-Pacific region. Indonesian coal demand is projected to grow by 4.6% per year, from 29 Mt in 2002 to 102 Mt in 2030.

Exports remain the driving force behind Indonesian coal production. Producers have a strong incentive to export coal, because export prices are higher than domestic prices, which are held down by the government. Exports have increased rapidly, from 1 Mt per year in the mid-1980's to 74 Mt in 2002. Indonesia is now the third-largest hard coal exporter in the world, after Australia and China. Exports are expected to reach 146 Mt by 2030, most of which will continue to go to the Asia-Pacific market.

Proven coal reserves in Indonesia total 5 billion tons, equivalent to 48 years of production at current rates, and are more than ample to meet projected domestic and export demand for several decades to come. It is not certain, however that the investment needed d to develop these reserves can be raised. The investment climate for coal producers and for coal service providers is clouded by transportation problems and by political, social, and economic instability. As a result, investment has slowed over the past few years. Economic nationalism further discourages inward direct investment in Indonesia. Foreign firms operating in the country's coal-mining sector are obliged to sell a majority stake to Indonesian companies within ten years of the start of production. This obligation recently led to litigation between the east Kalimantan provincial government and Kaltim Prima Coal, a 50-50 joint venture between Rio Tinto and BP, which produced about 18 Mt per year of steam coal for export markets. The case involved the pace of divestiture and the value of the stake. Rio Tinto and BP finally ended the dispute in 2003 by deciding to sell their entire stake, rather than just the 51% required by law. This dispute and others of its kind have discouraged foreign investment in Indonesia's coal sector and hence jeopardize the prospects for export growth. cl

|

|

Eastern Coal Council |

|

This

article is protected by United States copyright and other intellectual property

laws. The article may not be reproduced, rewritten, distributed, redisseminated,

transmitted, displayed, published or broadcast, directly or indirectly, in any

medium without the prior permission of Coal Leader, Inc. Copyright 2004, Coal

Leader, Inc. All rights reserved.